Quantum’s Commercialization Thesis Faces Its First Real Earnings-Season Stress Test

Defiance ETFs: Weekly Market Update | May 12, 2026

Hi everyone,

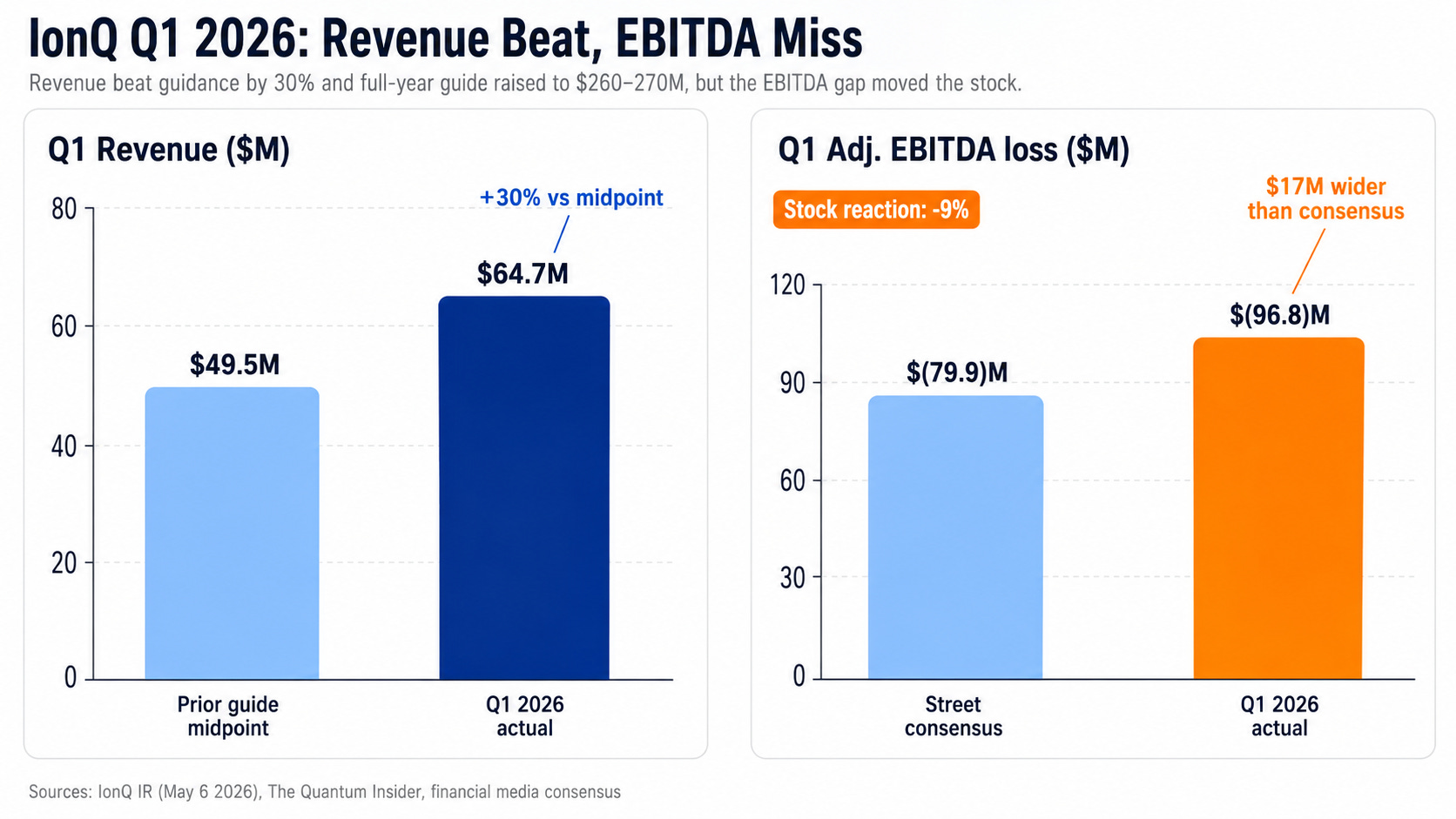

IonQ beat Q1 revenue by 30 percent, raised full-year guidance by roughly $30 million, and the stock fell 9 percent on the print. That gap is what the first real quantum earnings cycle of 2026 is teaching the market.

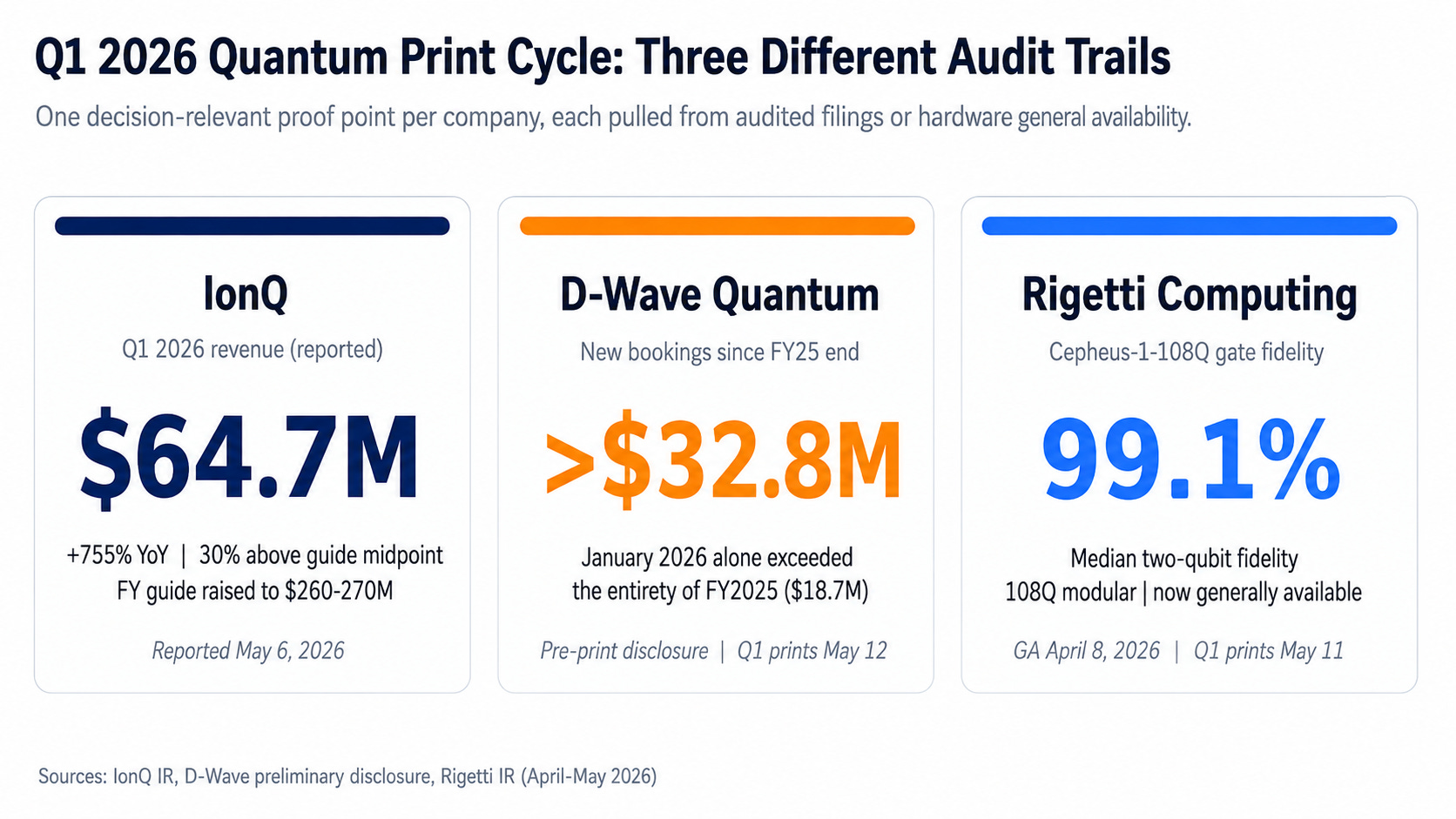

D-Wave reports Q1 this week having already disclosed more than $32.8 million in bookings closed since fiscal year-end 2025, with January 2026 alone exceeding the entirety of 2025. Rigetti reported Q1 this week on the back of Cepheus-1-108Q going generally available on April 8, a 108-qubit modular system at 99.1 percent median two-qubit gate fidelity.

For allocators reading the publicly listed quantum-computing companies reporting through this cycle, this is the cycle the sector has not had before. The 2025 thematic rallies were priced on press releases. The 2026 print cycle is priced on income statements, bookings cadence, and what management commits to in writing.

IonQ’s Print Is the First Real Stress Test of the Quantum Multiple

What caught my attention is the gap between the revenue line and the EBITDA line, and how the market chose to read it.

The $64.7 million top-line print is the largest quarterly revenue any pure-play quantum company has ever reported. Remaining performance obligations climbed to $470 million, up 554 percent year over year, which is the contracted backlog supporting the raised full-year guide. Government work anchors that backlog: a $39 million SDA HALO contract plus ongoing positions on the Missile Defense Agency SHIELD IDIQ and DARPA HARQ awards. The pending SkyWater acquisition, announced in January, pulls fabrication in-house at a moment when networking and packaging matter as much as qubit count.

The widening EBITDA loss is what the market wants to talk about. Management reaffirmed the full-year adjusted EBITDA loss range of $310 to $330 million, which means operating leverage is not expected to inflect inside 2026. That is the same friction AI infrastructure stocks worked through in 2023 and 2024.

Revenue traction is accelerating, but the path to operating leverage has to be visible before the market pays a steady multiple for the growth. The fact that quantum is being priced on that tension at all is the maturation signal.

IonQ beat Q1 revenue by roughly 30 percent and raised the full-year range, but the stock fell about 9 percent on a wider-than-expected EBITDA loss. Sources: IonQ IR, The Quantum Insider (May 6 2026)

Bookings, Not Press Releases, Are the New Currency

D-Wave’s pre-announced bookings figure is the more useful data point for reading the second-tier pure-plays. The company started fiscal 2026 with $18.7 million in bookings on the books for all of 2025 and has now closed more than $32.8 million in new bookings in roughly four months, with January alone surpassing the entire prior fiscal year.

The deals behind the number are not abstractions. A $20 million system sale to Florida Atlantic University and a two-year $10 million enterprise QCaaS commitment with a Fortune 100 buyer are exactly the customer-mix shift the QCaaS model needs. Consensus revenue for the quarter is modest, around $4 million, but bookings is the leading indicator for a recurring-revenue business. The call should clarify whether that cadence is showing up in deferred revenue and forward guidance.

Rigetti is the third data point. A 108-qubit modular system at 99.1 percent median two-qubit gate fidelity, accessible on Rigetti’s QCS platform and Amazon Braket, moves the conversation from roadmap commitment to commercial availability. Management has guided to 99.5 percent two-qubit fidelity later in 2026. The print should test whether Cepheus availability is pulling enterprise pilots into the revenue line.

The May print cycle delivers three different proof points: revenue cadence at IonQ, bookings velocity at D-Wave, and commercially available higher-fidelity hardware at Rigetti. Sources: IonQ IR, D-Wave preliminary disclosure, Rigetti IR (April-May 2026)

Photonics Becomes a Manufacturing Equipment Question

The other May development worth tracking is on the supply-chain side. Xanadu and EV Group announced a partnership on May 5 to develop heterogeneous integration and wafer-bonding processes for industrial-scale photonic quantum chip manufacturing. EV Group is the equipment supplier behind a large share of the advanced packaging steps the broader semiconductor industry already relies on.

Photonic quantum systems can in principle run through existing semiconductor foundries, but the heterogeneous integration step, bonding different materials at industrial volume, is the bottleneck between a working lab device and a manufacturable product. Pairing a photonic-quantum company with the equipment supplier the rest of the industry uses for that step is the closest thing to a manufacturing audit-trail event the photonics side of the sector has produced this year.

For allocators tracking the intersection of AI infrastructure and advanced manufacturing, the fabs, packaging vendors, and integration equipment scaling AI accelerators are the same suppliers the photonic quantum stack will draw on as it commercializes. The supply chain is more shared than the headlines suggest.

What This Cycle Sets Up

More prints land this week. Rigetti’s call tests whether Cepheus availability is converting to pipeline. D-Wave’s print tests whether the booked work is landing in deferred revenue and forward guidance. Xanadu follows on May 14.

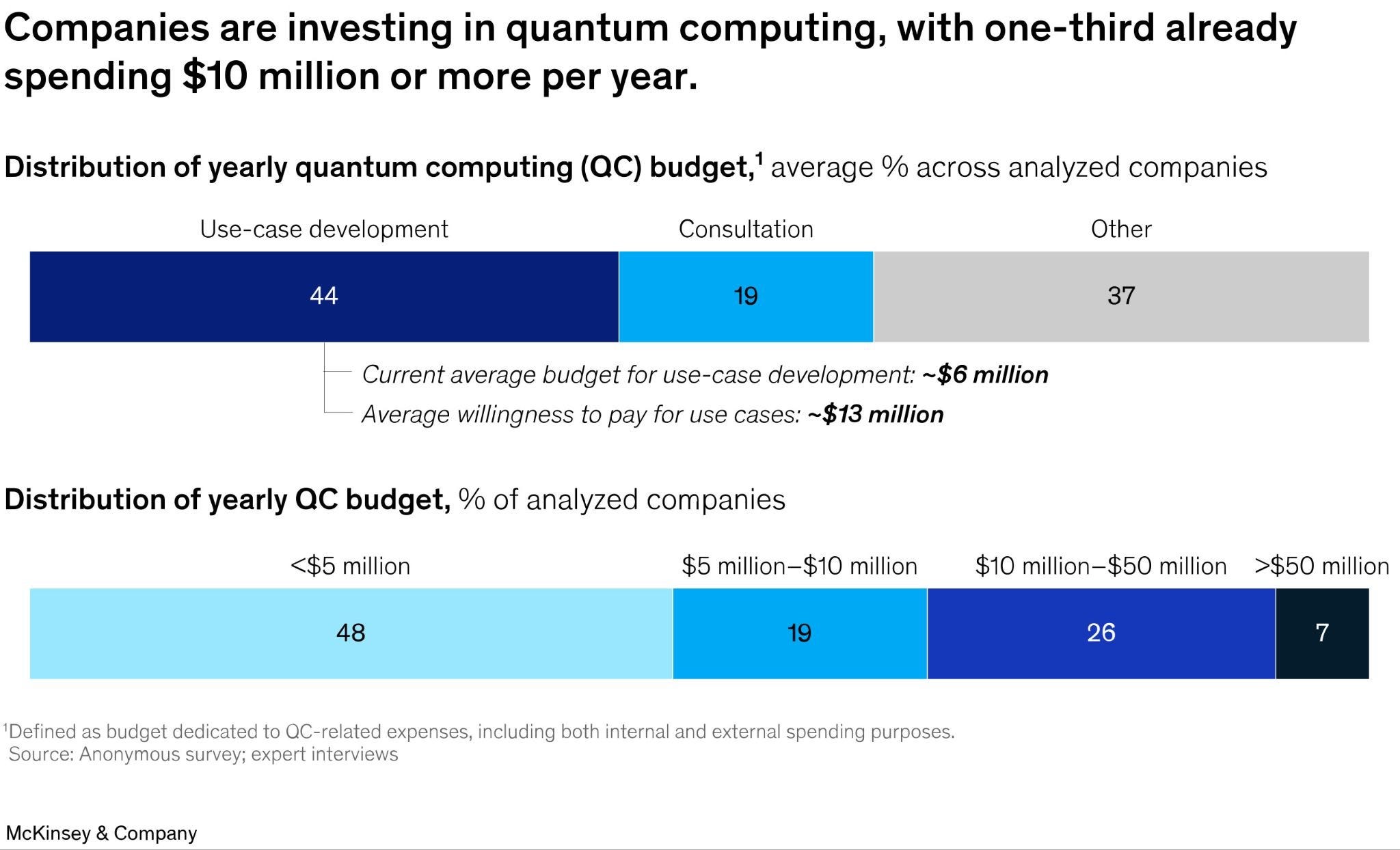

McKinsey’s 2026 Quantum Technology Monitor calls this the commercial tipping-point year. Roughly one-third of large global companies allocated more than $10 million to quantum in 2025, and 7 percent committed above $50 million. That enterprise spend needs a place to land, and the platforms reporting this week are the first cohort of public vehicles where allocators get to see whether it does.

The 7% of analyzed companies now committing above $50 million per year is the cohort most likely to anchor enterprise revenue at the platforms reporting this week. Source: McKinsey 2026 Quantum Technology Monitor

What I am watching is whether the cohort separates on the four axes that ultimately decide which infrastructure layers earn durable multiples: revenue cadence, operating leverage path, contracted backlog visibility, and manufacturing partnerships. IonQ has now put numbers against all four. D-Wave, Rigetti, and Xanadu each get their turn over the next several trading days.

Best regards,

Sylvia Jablonski

Defiance ETFs, CIO

Follow us on X (Twitter) | LinkedIn